The words we used to describe something tend to reflect the way we think about the subject.

For example, let’s say I’m walking down the street, and I see a rock lying on the sidewalk. If I describe that rock as a “loose chunk of gravel,” what image comes to your mind? Probably a craggy, rough, gray mound. But, if I describe the same rock as a “sharp, clouded, amber stone,” that creates an entirely different image.

Using one word in place of another can lead you to misunderstand the meaning that a statement is trying to convey. That can be a problem when we’re talking about a complex, high-level idea, like payments and fraud prevention.

Changing Terminology in the Payments Space

Payment card chargebacks were created in the 1970s as a “last resort” to protect consumers from fraud or dishonest merchants. If a cardholder notices an unauthorized charge show up on their monthly credit card statement, the cardholder can contact their issuing bank, who can file a chargeback to reverse the transaction.

eCommerce dramatically altered the dynamics of the merchant-customer relationship. However, the chargeback process has failed to keep up with the pace of change. Consumers can abuse the chargeback process, either on purpose or by accident, through a practice known as “friendly fraud.” This is a growing problem that could account for 60% of all chargebacks issued by 2023, according to internal data from Chargebacks911.

The good news is that card networks like Visa and Mastercard are picking up on this issue, at least to some degree. In 2018, Visa introduced the Visa Claims Resolution initiative, which was designed to weed out invalid customer disputes before they became chargebacks. The overall goal was to increase the efficiency of processing and resolving valid chargebacks.

As part of the initiative, Visa streamlined the types chargebacks allowed, as well as the reason codes used to identify them. They also made the decision to change certain terms in the chargeback process. For instance, the word “chargeback” was changed to “dispute,” while “representment,” the term used to describe the process of actually fighting a chargeback, became a “dispute response.”

The move was well-intentioned. After all, a chargeback does start with a customer dispute. It makes sense to carry a clearly linked designation across each stage of the chargeback process. However, merchants seem to be dragging their feet on really metabolizing the switch.

Merchants Having Trouble Making the Change

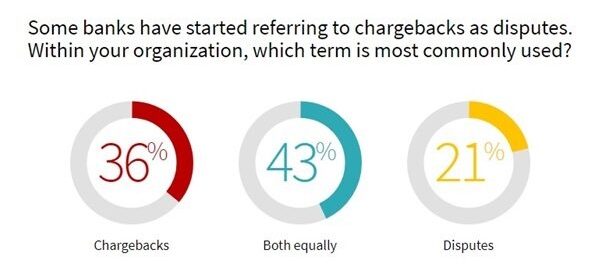

The recently published 2021 Chargeback Field Report shows that nearly 80% of merchants still use the word “chargeback” when referring to a Visa dispute. To further confuse the matter, more than one-third of merchants use the chargeback label exclusively. Closer to half of merchants say they use the terms “chargeback” and “dispute” interchangeably.

Image Source: Chargebacks911

The reasons for this vary. For starters, we’ve called it “the chargeback process” for decades. Merchants find it easier to stick with what seems familiar. Compounding this is the fact that the other major card networks—Mastercard, Discover, and American Express—continue to use the legacy terminology. This makes Visa the odd man out.

To make matters more confusing, merchants tend to use the term “dispute” to describe different things. Many of them refer to the representment process as “disputing a chargeback.” In other words, dispute can mean totally different things depending on the speaker and the card network in question.

It’s easy to see how misunderstandings can arise in this environment. And, when we’re talking about payments and fraud prevention, a misunderstanding can translate to missed deadlines, inefficiencies, and lost revenue for merchants.

We Need Standardized Terminology

The chargeback process is already difficult to navigate. Responding to a chargeback involves investigating the customer’s claim, compiling documentation, drafting a rebuttal, and submitting the information in the format required by the bank. Plus, in most cases, merchants have only a few days in which to do all this work.

Sellers are mixing up the terminology they use to refer to different steps of the dispute response. This can make an already-complex process even more confusing. That’s why it’s important to be clear on all terminology used.

We lack a standardized lexicon that’s accepted throughout the payments ecosystem. That doesn’t necessarily seem like a huge deal, but it can be a major obstacle.

To illustrate, imagine that a merchant is trying to research chargeback rules. The term they’re researching is not standardized, though, and two different card brands use the word in two different ways. This can lead the merchant to make choices in the representment process that end up costing them thousands of dollars. They might also deploy the wrong solution and waste even more time and money.

It can seem like I’m nitpicking here. The words we use to describe different facets of the chargeback process can’t really matter that much…can they? The truth is that they definitely can.

It Falls on Merchants’ Shoulders

Accuracy is important. That’s the bottom line.

The lack of standardized terminology and processes across different card networks throughout the payments process will, in many cases, translate to losses for merchants. Until we have greater standardization, merchants must make it a priority to know each card network’s chargeback rulesets and terminology, inside-and-out.

Merchants have to keep pace with any new changes. These typically come once or twice per year, with publication of a new chargeback guide for each card network. As of this writing, for instance, the most-recent edition of the Mastercard Chargeback Guide was issued on December 7, 2021. There will be other, minor updates here and there, though, which businesses need to keep tabs on.

Most importantly, merchants need to ensure that their risk management strategy reflects the moment in terms of chargeback and fraud risk factors. Until they accomplish this, no set of rule changes or technology updates will really address the surging problem of chargebacks and friendly fraud.

Digital & Social Articles on Business 2 Community

(74)