— May 24, 2018

Starting a new business is not for the faint of heart. It takes a great idea, hard work, a little luck and enough money to support operations. Over 20% of all new start-ups don’t survive the first year and less than 50% make it to their fifth anniversary; according to a recent USA Today report the number one reason businesses fail is they simply run out of cash. They were either under-capitalized at the start or underestimated how much money they would eventually need to fund operations or how long it would take to start generating revenue.

Ensuring you have enough money to run your business is critical to survival. And since you can’t manage what you can’t see, having an accurate, rolling 12 Month Cash Flow Forecast is a must for all new business owners. So what is a Cash Flow Forecast? It is an estimate of the amount and timing of all money that flows in and out of your business. Cash flows in to your business from your customers, bank loans and investors. Cash flows out of your business when you pay for expenses such as payroll, rent, utilities, taxes, supplies and loan payments. If more money is flowing into your business versus flowing out on a monthly basis, you are cash flow positive, and will have enough money to pay your bills and invest in growing your business. If more cash is flowing out of the business than coming in, you are cash flow negative, and will eventually run out of money, unless action is taken.

You don’t need an accounting background to create a simple cash flow forecast. In less than an hour per month you can create a simple spreadsheet that can be used to track money flowing in and out of the business. It will identify potential cash shortfalls before they happen so that you can manage them accordingly.

Creating a Simple Cash Flow Forecast:

Before creating a cash flow forecast for your business, it’s important to understand the timing of when cash flows in and out of your business each month. Do you have cash sales or do you sell on terms? If you sell on terms, what are your payment terms? Remember, 50% of all B2B invoices are paid late so be conservative when estimating when cash from accounts receivables will actually be collected. The same holds true for accounts payable. Do you get terms from your suppliers? If so, book the cash flowing out of the business when payment is due, not necessarily when you purchased the supplies or inventory.

Don’t let optimism factor into your forecast. Be conservative when projecting sales and receipt of payment. Book a 10% “Other” expense contingency into your forecast for unexpected expenses.

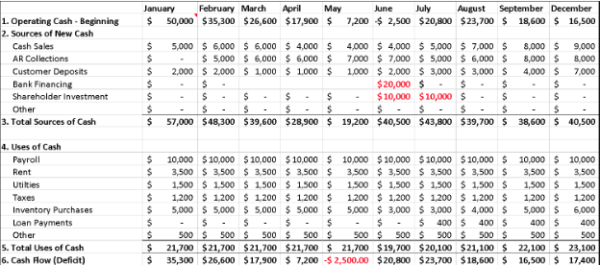

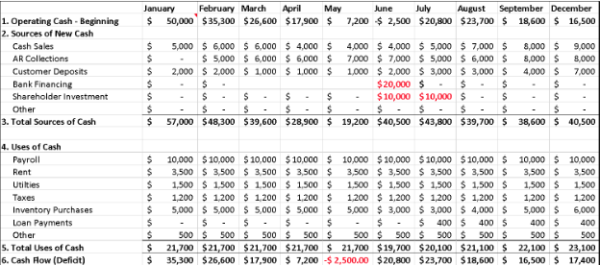

With realistic assumptions in hand, you can begin drafting your cash flow forecast. To get started, open a simple Excel spreadsheet and create 12 columns across the top of a spreadsheet, representing the next 12 months. Down the left-hand side, list the following cash flow categories:

- Operating Cash – Beginning: This is amount of money you’ll have at the beginning of each month. If you are just starting your business, this is the start-up capital on hand on day one.

- Sources of New Cash: All money coming in to the business each month including cash sales, AR collections, Customer Deposits, bank loans, new investments and any other sources of cash inflow. Use as many lines as you need. You can add lines as you develop new sources of revenue. Remember this is cash that will actually be received, not sales that will be collected sometime in the future.

- Total Sources of Cash: Add the amounts in 1. Operating Cash – Beginning, to all the amounts in 2. Sources of New Cash.

- Uses of Cash: List all expenses your business may incur, including payroll, rent and utilities, taxes, inventory purchases, loan payments, etc. Again, list only expenses that will be needed to be paid in that month. If you receive terms from your suppliers, book the cash outflow in the month when you will have to pay the Accounts Payable.

- Total Uses of Cash: Add amounts in 4. Uses of Cash so you can see exactly how much will be going out the door each month.

- Cash Flow (Deficit): This is the number that counts. Subtract 5. Total Uses of Cash from 3. Total Sources of Cash. If you see a positive number, you are cash flow positive and have enough money coming into the business to support operations and to invest back into your business. If you see a negative number for one of the months, it means you will be cash flow negative and actions must be taken to manage the situation. In the example above, the company is forecasting a cash flow deficit in May. It will need to secure a bank loan in June, and make additional shareholder investments in June and July in order to keep the business cash flow positive. Identifying a potential problem six months in advance will give you time to address the situation.

- Transfer the 6. Cash Flow (Deficit) to the 1. Operating Cash – Beginning row in the next monthly column and complete for the next 12 months.

As the months pass, compare your actual monthly cash flow statements to your projections for each month. If you see large differences from month to month, you need to adjust your projections and assumptions.

Update and Refine Your Projections on a Monthly Basis:

To keep your projections on track, create a rolling 12-month forecast plan that you update at the end of each month. Add a new month to the end every time a month is completed, so you will always have a year-long picture of your company’s financial situation. Adjust and refine it as your business grows and evolves.

Staying on top of your cash flow is critical to the success of your business. You face a number of challenges as a new business owner. You can avoid being blindsided by a sudden cash flow crisis if you take a few minutes each month to make sure the cash flowing out of your business does not exceed the cash flowing into your business.

Business & Finance Articles on Business 2 Community

(326)