To include search partners or not to include search partners? That is the question for many AdWords advertisers. To help answer this question, columnist Andy Taylor shares data on search partner ad performance.

The Google Search Network gives advertisers the ability to gain additional AdWords traffic and conversions from users across the web, as Google delivers ads on partner websites in much the same way it does on Google.com.

To target users searching on these partner sites, advertisers need only check a box in campaign settings to “include search partners.”

However, AdWords advertisers have long pined for a bid modifier to adjust bids for Google’s search partners, as the value of this traffic is often very different from that of clicks that come from users searching on Google.com. At the very least, it would be helpful if Google would allow advertisers to exclude specific search partners (as Bing Ads does).

While calls for additional functionality haven’t yielded results just yet, it hasn’t kept us from analyzing how these search partners are performing relative to Google.com. We’ve dissected the numbers to understand how performance looks for brand keywords, non-brand keywords and Shopping campaigns. And the results may surprise you.

Let’s start by talking about the current volume of search partner traffic to get a sense of how important the partner network is to paid search, then move into the value and cost of partner clicks.

Search Partner Share Flat To Down For Text Ads, Up For Product Listing Ads

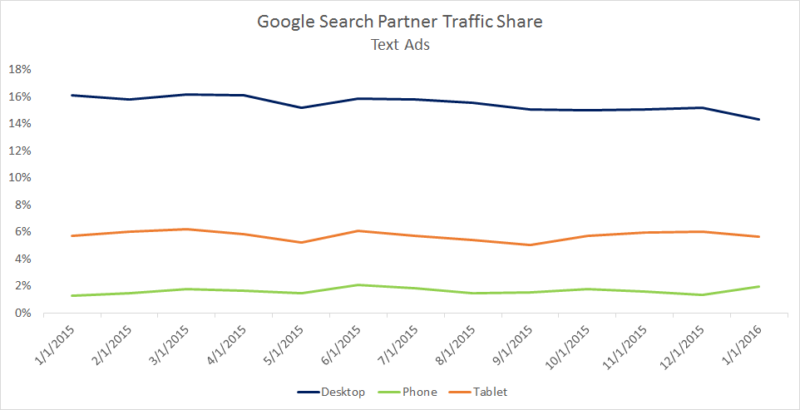

Taking a look at how the share of traffic coming from search partners has shifted over the past year, we see very different trends when looking at text ads compared to Product Listing Ads (PLAs).

On the text ad side, partner share saw no meaningful gains over the past 13 months.

There was an almost one-percentage-point drop on desktop computers from December to January, which is likely the result of AOL leaving Google’s network for Bing Ads at the beginning of 2016.

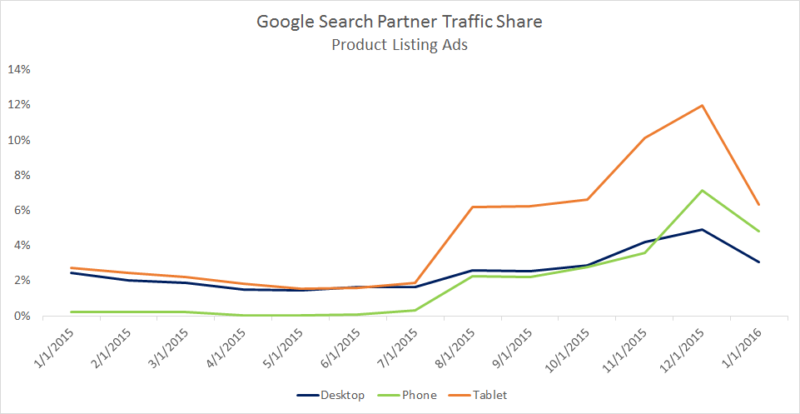

PLA search partner share, on the other hand, increased significantly beginning in August.

Google announced in late 2014 that large retail partners would be showing PLAs more often, and in the latter half of 2015, we started to see more paid search traffic from major retailers such as Kohl’s and Target. This drove up partner traffic share, particularly on mobile devices, during the holiday season.

Additionally, Google began showing PLAs for image searches on phones in December, with this traffic attributed to search partners in Google’s performance reports in the AdWords UI. Image search PLAs were also recently expanded to begin showing on desktop, as well.

While PLA partner share saw a serious decline from December to January across all device types, it remains significantly above the levels observed as recently as July of last year.

All told, across all device types and formats, search partners are now accounting for seven percent of all paid search traffic.

Now let’s take a look at how partner traffic is performing for advertisers, but not before mentioning a couple of caveats.

Caveat Time

Before reading further, it’s important to note the following:

- We do advocate for creating campaigns targeting keywords to Google.com only with higher bids than duplicate campaigns targeting both Google.com and the search partner network (which is admittedly convoluted and not feasible in all circumstances). The hope from this strategy is that most of the traffic from the campaigns that target both Google.com and the partner network will come from search partners in order to allow us to bid this traffic as effectively as possible, with the Google.com campaigns getting most of the Google.com traffic. However, this strategy did not significantly impact the performance of search partners relative to Google.com for the sample of advertisers studied for this analysis.

- The query mix of traffic on Google.com and search partners impacts relative conversion rate and cost per click (CPC). This analysis does not go into that, but rather just divides campaigns up into brand text ads, non-brand text ads and shopping campaigns for each advertiser in the sample.

Those points made, the following figures are based on median search partner performance versus Google.com performance for a set of more than 20 advertisers which target the search partner network with their campaigns. These are their stories (Law & Order sound).

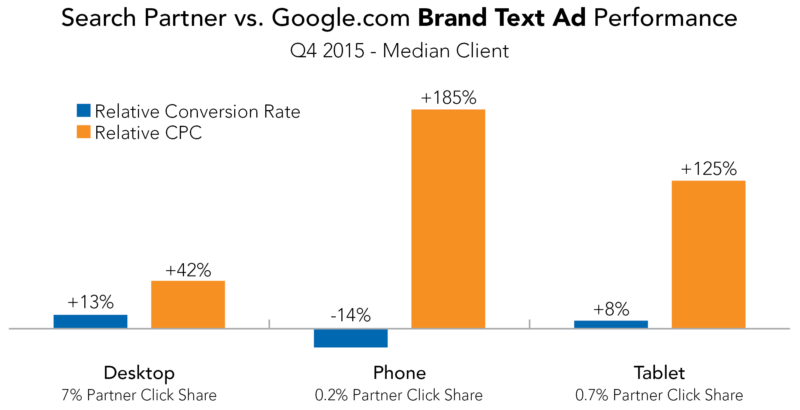

Search Partner Clicks Are MORE Likely To Convert Than Google.com Clicks For Brand Traffic

First, looking specifically at brand campaigns, search partner conversion rate is consistently higher than that of Google.com on desktop and tablet computers; in Q4 2015, conversion rates 13 percent and eight percent higher on desktop and tablet (respectively) for the median client.

While that’s probably a pleasant surprise for most advertisers, the downside is that cost per click (CPC) for search partner traffic is significantly higher than that of Google.com for brand terms. Thus, the cost per order is higher on search partners than on Google.com, despite partners returning higher conversion rates than Google.com on these devices.

On phones, conversion rate was 13 percent lower on search partners than on Google.com in Q4, while CPC was 185 percent higher. However, just 0.2 percent of brand phone traffic came from search partners.

As brand traffic usually converts at very high rates for most advertisers, search partners still maintain a great return on ad spend for these keywords, but it does speak to the need for more precise bidding controls that advertisers aren’t able to get the same return with the current system.

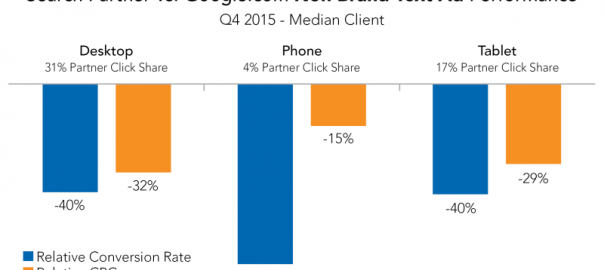

Non-Brand Text Ads: Return On Ad Spend For Search Partners Is Close On Desktop & Tablet, Not On Phones

When it comes to non-brand keywords, search partner conversion rate is significantly lower than Google.com conversion rate across all device types.

For desktop and tablet devices, CPC is 32 percent and 29 percent lower, respectively, on partners than Google.com compared to conversion rate being 40 percent lower on both devices. These figures are close enough that the overall return on ad spend isn’t far off for the median advertiser, and some advertisers do see search partner return on ad spend greater than that of Google.com.

Partners also make up a sizable share of non-brand text ad traffic on desktop and tablets, at 31 percent and 17 percent click share, respectively.

When it comes to phone traffic, conversion rate is 66 percent lower on partners than Google.com, but CPC is only 15 percent lower. That’s a pretty big difference, but fortunately, partners only accounted for four percent of all non-brand text ad traffic on phones.

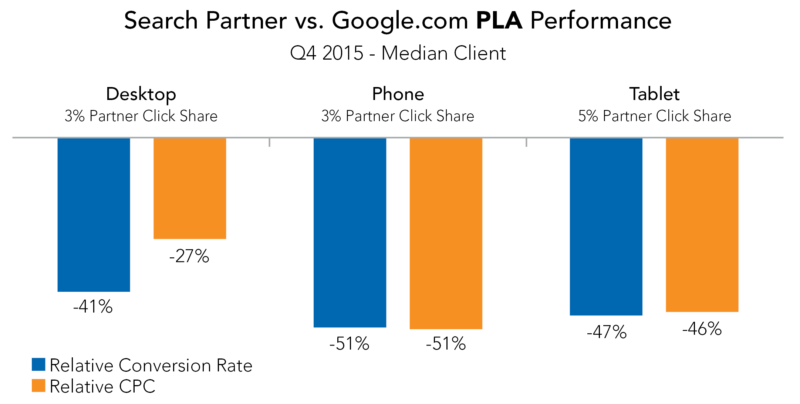

PLA Partner CPC & Conversion Rate Relative To Google.com Line Up Very Well On Mobile

Finally, partner PLA conversion rate and CPC produce a return on ad spend that’s almost identical to that of Google.com on phones and tablets.

As mentioned earlier, PLA traffic on mobile devices in particular picked up significantly at the end of last year, and it’s awesome to see this traffic providing value in line with the cost.

On desktop computers, conversion rate is 41 percent lower, but CPC is only 27 percent lower — a reasonable disparity to swallow in getting additional traffic and orders from these well-performing ads, but yet another example of why advertisers should be given controls to adjust bids for partner traffic.

Conclusion

Some might look at these figures and ask, “Why do these differences in performance exist?” I don’t have those answers, as Google’s search partner network is a bit of a black box. Do partners have first-page minimum bids and top-of-page minimum bids? If so, do those minimums differ from Google.com minimums? Is Quality Score calculated differently?

I don’t know, but these data do give you an idea of how partners perform compared to Google.com for a standard advertiser.

In looking at relative performance by device, ad format and keyword brandedness, there are areas where return on ad spend lines up very well across Google proper and its search partners for the median advertiser. There are also areas where there appear to be some pretty clear inefficiencies.

Some advertisers do see better return on their partner spend than on Google.com spend, and there are also those that see significantly worse relative partner performance than the differences shown in the numbers in this post. Only by targeting the partner network and collecting data can you decide how that plays out in your own campaigns.

As always, advertisers want more control over the performance of their accounts. Whether Google will hand over that control remains to be seen, but I hope this analysis provides you with some framework on how to think about whether you should be targeting the partner network with your campaigns.

[Article on Search Engine Land.]

Some opinions expressed in this article may be those of a guest author and not necessarily Marketing Land. Staff authors are listed here.

(Some images used under license from Shutterstock.com.)

Marketing Land – Internet Marketing News, Strategies & Tips

(83)